A Journal of Foreign Policy Issues

These energy resources and, in particular, the oil

and natural gas deposits have now become the apple of discord in Central Asia introducing, according to analysts, a new chapter in the ĂGreat GameĹ (1) of control over Eurasia.

and natural gas deposits have now become the apple of discord in Central Asia introducing, according to analysts, a new chapter in the ĂGreat GameĹ (1) of control over Eurasia.

Although the stakes involved remain the same, i.e., power, influence, security, wealth, the new playing field is further complicated by an array of problems. These include intra-regional conflict, political instability, fierce competition among multinational conglomerates, and a shortfall in commercial expertise and legal infrastructures (2).

Moreover, the fact that the three countries which share the majority of the regionĹs energy and resources, namely Kazakhstan, Azerbaijan and Turkmenistan, are landlocked makes them depend on their immediate neighbours for access to the Western markets.

The essence of this new geopolitical game in Central Asia is twofold: first, control of production of the oil and gas, and second, control of the pipelines which will transfer the oil to the Western markets (3).

From a geopolitical point of view, Central Asia has always been important (4). From the middle to the end of the 19th century, while the region was part of the Russian Empire, the oil-bearing areas of Baku were producing half of the worldĹs oil supplies (5). In World War II, during his campaign against Russia, Hitler tried to capture Baku and the Caucasian oil fields as part of his strategy for world domination. After the war, the Soviets retained these areas as reserves, choosing to exploit oil deposits on Russian soil, in Tatarstan and Siberia (6).

Following the collapse of communism,

the ex-Soviet republics of Central Asia, especially Azerbaijan and Kazakhstan, have been trying to exploit their natural resources, since they consider oil to be the prime means of securing their economic and political independence. According to the estimates of geologists, the oil deposits of the Caspian Sea may not be quantitatively comparable to the deposits of the Persian Gulf, but they are still considered of excellent quality and able to provide a significant alternative source of energy in the 21st century (7). In particular, it is estimated that the entire Caspian Sea is a basin full of oil and natural gas, starting from Azerbaijan and continuing to the opposite shore in the territory of Kazakhstan and Turkmenistan. These deposits take on enormous importance because of the expected exhaustion of the deposits of Alaska and the North Sea by the year 2015.

the ex-Soviet republics of Central Asia, especially Azerbaijan and Kazakhstan, have been trying to exploit their natural resources, since they consider oil to be the prime means of securing their economic and political independence. According to the estimates of geologists, the oil deposits of the Caspian Sea may not be quantitatively comparable to the deposits of the Persian Gulf, but they are still considered of excellent quality and able to provide a significant alternative source of energy in the 21st century (7). In particular, it is estimated that the entire Caspian Sea is a basin full of oil and natural gas, starting from Azerbaijan and continuing to the opposite shore in the territory of Kazakhstan and Turkmenistan. These deposits take on enormous importance because of the expected exhaustion of the deposits of Alaska and the North Sea by the year 2015.

The Issue of Production

Azerbaijan

Azerbaijan belongs to one of the areas of the world richest in oil

and has a long history in the production of oil and natural gas. Despite its age-old production, Azerbaijan still possesses considerable oil deposits, which have remained unexploited. During the 20th century, the oil industry in Azerbaijan drew oil from the deposits in the countryĹs land subsoil, while offshore development began only in the middle of our century, and at a small depth. The first major offshore oilfield from which oil was drawn was the ĂOil RocksĹ, in 1949. When this source was exhausted, it was replaced by another offshore oilfield, the ĂGuneshliĹ, which was discovered in 1980 and by 1991 covered 57% of AzerbaijanĹs output. In addition, offshore exploration for oil deposits in the Caspian Sea had already borne fruit in the 1980s with the discovery of three major oilfields - ĂChiragĹ, ĂAzeriĹ, ĂKapazĹ - at great depth (8).

and has a long history in the production of oil and natural gas. Despite its age-old production, Azerbaijan still possesses considerable oil deposits, which have remained unexploited. During the 20th century, the oil industry in Azerbaijan drew oil from the deposits in the countryĹs land subsoil, while offshore development began only in the middle of our century, and at a small depth. The first major offshore oilfield from which oil was drawn was the ĂOil RocksĹ, in 1949. When this source was exhausted, it was replaced by another offshore oilfield, the ĂGuneshliĹ, which was discovered in 1980 and by 1991 covered 57% of AzerbaijanĹs output. In addition, offshore exploration for oil deposits in the Caspian Sea had already borne fruit in the 1980s with the discovery of three major oilfields - ĂChiragĹ, ĂAzeriĹ, ĂKapazĹ - at great depth (8).

The problem was that, even though the Soviet oil industry had successfully developed its offshore oilfields and was even among the pioneers in this field, it had done so through virtually primitive means. The Soviet oil industry was never technologically able to develop offshore oilfields at great depth. Thus, AzerbaijanĹs offshore oilfields have remained, to a large extent, undeveloped. AzerbaijanĹs government has invited major foreign oil companies possessing the necessary technology, capital and project organisation to develop its offshore fields (9). The three biggest Azeri oilfields are being developed by the Azerbaijan International Operating Company, a twelve-company consortium which includes BP and Amoco (10).

The negotiations on the development of these oilfields involve complex legal, technical and commercial issues. The most important problem is the lack of a legal framework for the development and exploitation of AzerbaijanĹs oil. Furthermore, the restructuring of the domestic oil industry and negotiations with foreign companies have been hampered by the frequent changes of government. In order to improve the prospects for foreign investment, Azerbaijan is considering the adoption of a more flexible legal framework on oil contracts. Within this context, the government of Azerbaijan founded in August 1992 a public oil company adopting the norms of modern international oil companies. Every negotiation with foreign companies is conducted through this government company, while the development of joint stock status is being considered.

In order to conform to international practice and complete the negotiations as soon as possible, the government of Azerbaijan has also sought the advice of experienced international consultants (11).

Apart from the development of the oilfields, which has already begun, Azerbaijan continues its explorations for other deposits in the Caspian Sea. In the part of the Caspian belonging to Azerbaijan, around 24 sites have been singled out as suitable for drilling.

It is obvious that the development of the energy sector will have beneficial effects on AzerbaijanĹs economic development, in general. The prospects of AzerbaijanĹs energy sector will depend on whether new projects for the exploitation of the new deposits under the seabed prove to be satisfactory. The oil balance sheet is expected to show improvements compared with the current year, particularly if the exploitation of the ĂGuneshliĹ oil field continues unobstructed. In the long run, total oil production is expected to reach 25.6 million tons per year in the year 2000 and 45.2 million tons in 2005, by which time the exploitation of other offshore deposits will have begun. Since domestic consumption is not expected to rise significantly, the total quantity of oil for export is expected to reach 20.8 million tons in 2000 and 39.7 tons in 2005 (12).

Kazakhstan

Kazakhstan, ranking second -after Azerbaijan- among the oil-producing countries of the former Soviet Union, also commands abundant energy resources. Because of the countryĹs position, the transit routes and oil pipelines, Kazakhstan exports oil mainly to the Russian Federation (13). Oil represents 15% of KazakhstanĹs total exports. If the programme of reforms and the pace of foreign investments proceed according to schedule, it is estimated that in 1998 oil will account for 60% of KazakhstanĹs exports (14).

Kazakhstan has tried to attract foreign investors with advanced technology and expertise for the extraction of these deposits. A large number of foreign investments are already in progress in Kazakhstan. The most important ones include the agreement with Chevron to develop the oilfield of Tengiz, in western Kazakhstan, and the agreement with a consortium which includes British Gas, Agip and Texaco, to develop the Karachaganak field in northern Kazakhstan (15). ChevronĹs investment in Tengiz began in 1993 and, when completed, it is expected to come up to the level of 20 billion dollars. The investment of the British Gas/Agip consortium is of approximately the same size. The completion of these investments will have important consequences for the oil exports and the economic development of Kazakhstan.

The government of Kazakhstan is also examining various alternative proposals for the construction of an oil pipeline which will channel the oil to the West. The most feasible proposal seems to be the one that entails the upgrading of the existing network which traverses the area around the northern part of the Caspian Sea, ending at the port of Novorossisk, in conjunction with the modernisation of the facilities of this Russian port. This solution entails close Cupertino with Russia and Azerbaijan. Other proposals under examination include an oil pipeline, which will cross the Caspian Sea, Azerbaijan and Georgia to end at a Turkish port. Another proposal, which was turned down after American pressure, involved an oil pipeline which would cross Iran, ending in the Persian Gulf.

With regard to the financing of the oil pipelines, meetings are being held and promises made by the World Bank, the International Monetary Fund and the European Bank for Reconstruction and Development. The construction of the new pipeline or the upgrading of the existing network for the channelling of oil to the West will undoubtedly be the key to the countryĹs economic development.

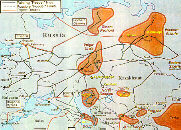

The issue of pipelines

With deals to develop the oilfields in Azerbaijan and Kazakhstan already signed, the biggest problem facing foreign investors is how to transport the oil to foreign markets. Unlike other big oil producers, Azerbaijan and Kazakhstan are landlocked. The issue of pipeline selection has therefore acquired enormous geopolitical significance for the future of the region. The existing pipeline routes for oil from Azerbaijan and Kazakhstan ran through Russia to the port of Novorossisk on the Black Sea, giving Moscow a considerable advantage in the process of pipeline selection (16). Following the agreement between Chevron and Kazakhstan, Moscow initially refused to allow crude oil through its pipeline system. It later placed restrictions on the amount of oil which could be transported through its pipelines and imposed a series of high tariffs. All these manoeuvres resulted in a deal which allowed Russia to become member of the Caspian Pipeline Consortium, which will build a $2 billion pipeline from Kazakhstan to Novorossisk.

The Azerbaijan International Operating CompanyĹs Ăearly oilĹ is being transported along two routes which for the most part use existing pipelines: a northern route through Dagestan and Chechnya to Novorossisk, and a second western route to the Georgian port of Supsa. Oil is already flowing along the northern route, and so far, the Chechens have been bought off with substantial transit fees (17).

These pipeline arrangements are temporary solutions dealing only with the transport of the early oil. The final decision regarding the selection of the pipelines which will carry the main oil is expected sometime in 1998. In theory, new pipelines could go in almost any direction. Northern routes could enhance the existing network and serve RussiaĹs needs. Western routes could serve Europe, while southern or eastern routes could serve the Asian markets (18).

The main options are the following: (19)

1. The northern route favoured by Russia. According to this option, Kazakhstan would expand its existing pipelines to link them to the Russian network and Azerbaijan would build a pipeline from Baku to Novorossisk. The shortcomings of this option have to do with fears of establishing excessive Russian control over the pipeline and also the issue of security, since the pipeline would go through Chechnya.

2. The western route favoured by Azerbaijan, Turkey, Georgia and the United States. This pipeline route would bring the oil to the Georgian port of Supsa and then ship it through the Black Sea and the Bosporus to Europe. Turkey insists that the straits cannot cope with increased tanker traffic and has proposed, instead, to construct a pipeline from Baku to the port of Ceyhan on the Turkish Mediterranean coast. However, excessive costs (around $2.9 billion) and serious security concerns (this route would pass through unstable Kurdish territory) make this option difficult to implement. Instead, the Bosporus could be by-passed by a pipeline linking the Bulgarian port of Burgas with the Greek port of Alexandroupolis.

3. The southern route. Economically, this is the most viable option, since Iran already has an extensive pipeline system, and the Gulf is a good exit to the Asian markets. The United States, however, has practically vetoed this option.

4. Eastern route. This pipeline would transport oil from Kazakhstan to China. It will be the costliest pipeline (covering 2,000 km in Kazakhstan alone) but the Chinese consider it as a strategic decision and are willing to implement it.

5. South-eastern route. The American oil company Unocal has proposed the construction of oil and gas pipelines from Turkmenistan through Afghanistan to Pakistan and later to India. This route makes sense geographically but not politically, since it will have to go through unstable Afghanistan.

The final decision about the pipeline or the pipelines which will transport the Caspian oil will be taken sometime in 1998 and is hard to predict in view of the multiplicity of options and competing interests. Given the strength of the Russian and American support for the northern and the western routes respectively, these pipelines seem to have an advantage over the others.

The Policies of the Great Powers in Central Asia

US Foreign Policy

The structure of the oil industry in the West changed radically and perhaps permanently in 1973. Control of the worldĹs oil resources shifted from the big multinational oil companies to a small number of oil-producing countries, most of them members of OPEC. The oil crisis of 1973-4 and the two increases in oil prices which followed, one in 1973 and another at the end of the 1970s, forced the countries of the West to reshape their policy on energy by emphasising alternative sources of energy. Despite that fact, the fall in oil prices in the 1980s, as these could not have remained at the high levels of the 1970s, increased demand and oil imports. Thus, while in 1973 world oil consumption was 57 million barrels a day, in 994 it approximated to 68 million barrels (20).

The USA leads the world in oil consumption, with 17 million barrels a day in 1991. Of this quantity, 50% is imported, so that dependence on oil imports is expected to rise steadily in the next decade. Even though US government committees, examining the issue, have found that dependence on oil imports threatens US national security, American oil policy has not changed radically with regard to imports. These findings have not led to the formation of a new oil policy which would aim at the progressive reduction of oil imports. They have, however, led the American Government to seek diversification of supply, to avoid dependence on a single supplier or team of suppliers. The addition of new exporters, such as Kazakhstan and Azerbaijan, to the already existing oil-producing and exporting countries provides more freedom of choice for importing countries such as the US, while it also helps to keep oil prices down (21).

Within this framework, one can explain the American interest in the restructuring of the Russian oil industry as well as in participation in the development of oilfields in the Caspian Sea and the surrounding countries. These oil deposits constitute new sources of supply from countries outside the OPEC and are, for this reason, extremely important on the political as well as on the economic level. The Caspian Sea basin has attracted US interest for the following reasons:

1. The oil of this region is considered to be of good quality.

2. The biggest part of this oil is intended for export, since the needs of the producing countries are relatively low and are expected to remain low.

3. The fact that the countries of the region lack the capital and the technology to proceed independently to the development of these oilfields offers American companies, such as Chevron, considerable investment opportunities.

In this context, we can better understand the geopolitical and economic aims of the US in Central Asia. At the geopolitical level, the United States wants to help the countries of Central Asia to develop their oil and natural gas industries. According to the estimates of the American Government, this development will bring about economic growth and will help these countries move away from the Russian sphere of influence.

At the economic level, the development of the oil industry of these countries means investment opportunities for the American construction and oil companies. Politically, the United States will be in a position to control these new important energy resources and diversify its own sources supply. American private companies have been supported by the US Government in at least two countries of Central Asia, namely, Kazakhstan and Azerbaijan. Other American political objectives include the containment of Iran and the reinforcement of TurkeyĹs role in the region. The US has not only blocked any pipeline route passing through Iran, but has also cancelled IranĹs participation in the international consortium which has undertaken oil production in Azerbaijan (22).

To sum up, US foreign policy in Central Asia is founded on the following rationale:

Russia

At this point it should be mentioned that control over these energy resources has set off a smouldering rivalry between Russia and the US which has two dimensions: the first concerns control of oil production and the second specific questions relative to the legal status of the Caspian Sea. Russia claims that the Caspian is an inland lake and not a closed sea, which means that it is not subject to the Law of the Sea. Consequently, exploitation of the Caspian resources must be subject to an agreement among all five coastal states.

Azerbaijan and Kazakhstan maintain that the Caspian Sea is just that, a sea, and as such should be divided into national sectors. The US holds the same position and it recently took a firm stand on the issue. Glen Rase, the director of international energy policy at the US State Department, declared in March 1995 that each of the countries in the region has the right to develop its own economic resources according to its own best interests... and there should be no misunderstanding. The US recognises legitimate security concerns, but does not recognise spheres of influence. The US will defend its companiesĹ interests in the Caspian (23). In this context the American Government has supported the private companies which have undertaken production on behalf of the former Soviet republics of the Caspian Sea. The United States wants to avert Russian control over the Caspian energy resources and will resist it as much as possible.

Russia, on the other hand, is concerned with the attempts to oust it from its traditional sphere of influence but is also worried that investment in the Caspian Sea oilfields will divert Western financial backing and interest from its oilfields in Siberia and the Far East and capture some of its market. In the competition over Caspian oil, therefore, Russia sees both the erosion of its geopolitical position and the loss of key economic resources and their potential revenues (24).

MoscowĹs initial response was an effort to strengthen the framework of the Commonwealth of Independent States, but this was not successful. Russia is now trying to find ways to deal with its competitors. In this context it has recently co-operated with Iran to offset AzerbaijanĹs and KazakhstanĹs claims in the Caspian and has participated in the construction of the Burgas-Alexandroupolis pipeline in an effort to by-pass Turkey.

In the past, the Soviet Union rarely used oil and gas exports to support her national interests. These exports were viewed as the countryĹs best earners of hard currency and nothing more. That approach seems to be changing. Russia has become much more aware of the geopolitical role that energy can play. She intends to use her oil and gas strength as a means of supporting foreign policy aims (25).

It is quite evident that there can be no game unless Russia is invited to the table. Giving Russia a seat at the table means equity participation both in pipeline construction and operation and in oil development projects (26).

Concluding Remarks

Energy resources are reshaping the geopolitical map in Eurasia. Eventual control of the development of oil deposits as well as the eventual pipeline routing will determine the political and economic future of Russia, Turkey and the Central Asian states; it will determine IranĹs position in the region and its relations with the West; it will determine the realignment of the strategic triangle among the US, Russia and China; and it will have strategic consequences by lessening dependence on Persian Gulf oil.

The importance of the eventual pipeline routings was pointed out by the Russian newspaper ĂIzvestiyaĹ: The struggle for future routings of oil from CIS countries to the world market is entering a decisive stage. The victor in this struggle will receive not only billions of dollars annually in the form of transit fees: the real gain will be control over pipelines, which will be the most important factor of geopolitical influence in the TransCaucasus and in Central Asia in the next century (27). n

1. The phrase Great Game has been borrowed from Rudyard KiplingĹs description of the rivalry between Tsarist Russia, Victorian England and the Ottoman Empire in Central Asia for control of trade routes to India in the 19th century. See Fiona Hill, Pipeline Politics, Russo-Turkish Competition and Geopolitics in the Eastern Mediterranean in Security and Cooperation in the Eastern Mediterranean, edited by Andreas Theophanous and Van Coufoudakis. (Cyprus: Intercollege Press, 1997), p. 200.

2. Rosemarie Forsythe, The Politics of Oil in the Caucasus and Central Asia, Adelphi Paper, No 300, (May 1996), p. 6.

3. While the Central Asian states have physical possession of their oil and gas reserves, they do not possess the capital and the technology that would allow them to go into production alone, a fact which brings in the foreign companies with a share in production and revenues.

4. Colin S. Gray, The Geopolitics of the Nuclear Era: Heartland, Rimlands, and the Technological Revolution (New York: Crane, Russak and Co., 1977).

5. The Rothschilds, and the Nobel Brothers, first provided Russia with the know-how to develop the Caspian oil resources. See Robert W. Tolf, The Russian Rockefellers, (Stanford, CA: Hoover Institution Press, 1976), pp.50-60.

6. Daniel Yergin, The Prize: The Epic Quest for Oil, Money and Power (New York: Simon & Schuster, 1991).

7. Proved and inferred reserves are estimated to be as high as 200 billion barrels, putting the region on a par with Iraq. In addition, the area is rich in natural gas with estimated and proved reserves of up to 7.89 trillion cubic metres - as much as those of the US and Mexico combined. Rosemarie Forsyth, The Politics of Oil in the Caucasus and Central Asia, p. 6. The Caspian Sea oil cannot compete with Persian Gulf oil in terms of easy access to the major world markets, nor will this oil be able to compete in terms of levels of production or costs of production. Once the production of the Caspian region reaches its peak - and that will be of the order of several million barrels per day - its contribution to the world oil supply may not be decisive but it will certainly be important. These reserves are significantly bigger, for example, than EuropeĹs proved reserves of about 50 billion barrels of oil equivalent. See Robert E. Ebel, The Dynamics of Caspian Sea Resources, paper presented to a Conference on Conflict Resolution, organised by the Institute of International Relations, Panteion University, on Corfu on 30-31 August 1996. Also see Central Asia: A Survey, The Economist, (7-13 Feb. 1998), p.6.

8. Azerbaijan: Energy Sector Review, Document of the World Bank, Report No. 12061-AZ (World Bank,Washington DC, 1993).

9. For these oil companies, the Caspian holds a further attraction. Unlike the majority of the worldĹs proved oil reserves, these resources are available for exploitation by Western firms. Iran and Iraq, the underdeveloped giants of the Persian Gulf, are closed to outsiders, so for the moment the oil firms are concentrating on the Caspian. Central Asia: A Survey p. 6.

10. Ibid.

11. Azerbaijan: From Crisis to Sustained Growth, A World Bank Country Study (The World Bank, Washington DC, 1992).

12. Azerbaijan: Petroleum Technical Assistance Project, Document of the World Bank (The World Bank, Washington DC, 28 March 1995).

13 Kazakhstan: The Transition to a Market Economy, A World Bank Country Study (The World Bank, Washington DC, 1993).

14. Ibid.

15. Central Asia: A Survey, The Economist, p.6.

16. Ebel, p. 6; Hill, p. 209, The Economist, p. 6.

17. Central Asia: A Survey, p. 8.

18. Ibid, p. 8.

19. For a detailed analysis see Rosemarie Forsythe, The Politics of Oil in the Caucasus and Central Asia, pp. 44-55; Central Asia: A Survey, pp. 8-9.

20. Robert E. Ebel, Petroleum: A New Factor in the Black Sea Security Context, unpublished paper presented to a conference on Security and the Black Sea, held in Varna, Bulgaria, 9-10 May 1995; Robert E. Ebel, Michael P. Croissant, Joseph R. Masih, Kent E. Calder, Raju G.C. Thomas, Policy Forum: Energy Futures, The Washington Quarterly, Vol. 19, No. 4 (Autumn 1996): 71-99.

21. Ibid.

22. Ibid, p. 6; Rosemarie Forsythe, The Politics of Oil in the Caucasus and Central Asia, p. 55-58; Hill, Pipeline Politics, pp. 212-217.

23. Ebel, Petroleum: A New Factor in the Black Sea Security Concept p. 7; John Lloyd, Battle Lines Drawn Over Caspian Oil and Gas, Financial Times, 3 March 1995.

24. Hill, Pipeline Politics, p. 216.

25. Ebel, p. 9.

26. Ebel, The Dynamics of Caspian Sea Resources, p. 8.

27. Ebel, p. 9.